As I sit on my front porch tonight, I find myself reflecting on this summer day exactly one year ago when the state I proudly call home was pelted several days and nights in a row with thunderstorms and heavy rainfall, resulting in some of the worst flooding West Virginia has ever seen. Ironically, it’s raining tonight, and the forecast for the week ahead calls for more rain. I can’t help but wonder how many of my neighbors may also be praying for sunny days and hoping for respite this time.

On the eve of the June 2016 floods anniversary, I thought it fitting to highlight the protection of flood insurance and how the coverage is often misunderstood. My office received many calls both during and after the flooding last year. We counseled, we worked hard, we prayed, we cried, we cleaned up our community, and along with our fellow mountaineers, we came together. During this time, it became painfully apparent to us that many folks believed they had the coverages they needed when in fact, they did not. To quickly share pertinent information, I made a brief Facebook post. It was shared several times, and the information was so sought after that I decided to expound upon it here.

FEMA regulates flood insurance. According to FEMA’s website, a flood is simply an excess of water on land that is normally dry. Per the National Flood Insurance program, a flood is (1) “A general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (at least one of which is your property) from a. overflow of inland or tidal waters; b. unusual and rapid accumulation or runoff of surface waters from any source; or c. mudflow*. (2) collapse or subsidence of land along the shore of a lake or a similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood as defined in A.1.a. above.”

A few facts about flood insurance you should know are:

- Often, flood insurance policies come with a 30 day waiting period. This is waived if a lender requires the coverage during the initial purchase or refinancing of a loan.

- Flood insurance CAN cover contents, but that coverage must be purchased separately, and the limit of coverage must be selected. *Side note: A lender does not require you to purchase contents coverage, only coverage for what is financed—typically just the structure. If contents coverage is needed, you must add this with your agent! *

- Flood insurance is not a valued policy. “A valued policy pays the limit of liability in the event of a total loss. For example, Your home is destroyed by a fire, and it costs $150,000 to rebuild it. If your homeowners’ insurance policy is a valued policy with a $200,000 limit of liability on the building, you will receive $200,000. Flood insurance pays the replacement cost or ACV (actual cash value) of damages, up to the policy limit.” (www.FEMA.gov).

- Coverage is limited in the lowest elevated floor and basements. Therefore, if you live in a flood zone, you must be extremely careful about what you choose to store in that part of your house.

- Personal property is usually covered at actual cash value, NOT replacement cost on a flood insurance policy. Consider this strongly when purchasing a home in the flood zone.

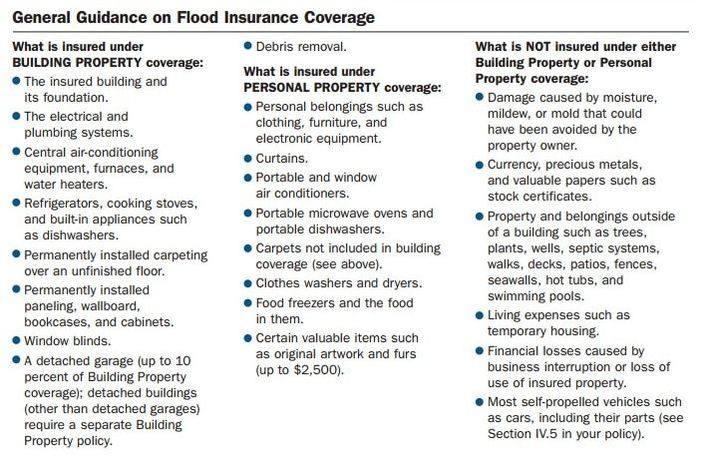

Below is a helpful illustration from FEMA on what IS covered by flood insurance and what is NOT.

As I conclude this post and listen to the steady rainfall, I am reminded of the incredible power of water when it accumulates and accelerates through our West Virginia hills and valleys. I’m also reminded of an even more powerful God who holds each of us in the palm of His hand as we find our rest. May we all be mindful of our neighbors, especially tonight and of the community, spirit, and passion we share as West Virginians.